Find out how these notes have a potential to provide a fixed coupons while also providing contingent principal protection.

CIBC Investor’s EdgeJul. 26, 2025

3-minute read

Share

What are autocallable coupon buffer notes?

Autocallable coupon buffer notes are a structured investment product that is type of Principal At Risk (PAR) note. They have the potential to provide periodic fixed coupons (typically on a semi-annual basis) linked to the performance of a reference asset while also providing contingent principal protection at maturity.

These notes have a call feature where the note can be automatically called if the reference asset return is above the predetermined call threshold level on a valuation date (typically observed on an annual or semi-annual basis).

If a note does not get called prior to maturity, the investors original principal is fully protected as long as the reference asset return is above the predetermined downside buffer at maturity.

Key features

Investors have the potential to receive their initial investment and predetermined fixed coupon(s) prior to the maturity date of the note.

Investors have contingent principal protection at maturity.

Key benefits and considerations

The returns of autocallable coupon buffer notes are based on the performance of an equity, commodity, currency or basket thereof (the reference asset).

The fixed coupon is paid to investors as long as the reference asset return is above the coupon threshold on a valuation date (typically observed on annual or semi-annual basis).

The call feature of the notes is based on a predetermined call threshold. If the reference asset return is above the call threshold on a valuation date during the term of the note (or the maturity date), the note will automatically be called by CIBC and the investors will receive their initial investment, in addition to the coupon payment.

The contingent principal protection of the notes is based on a predetermined downside buffer percentage. If, at maturity, the reference asset return is negative but is still at or above the downside buffer, investors will receive an amount equal to their initial investment. If, at maturity, the reference asset return is negative and the downside buffer was breached (reference asset declined by more than the buffer percentage), the investors bear the loss by the amount the reference asset return is less than the downside buffer percentage, multiplied by a participation factor. In these situations, investors will sustain a loss of a portion of their initial investment.

Payout overview

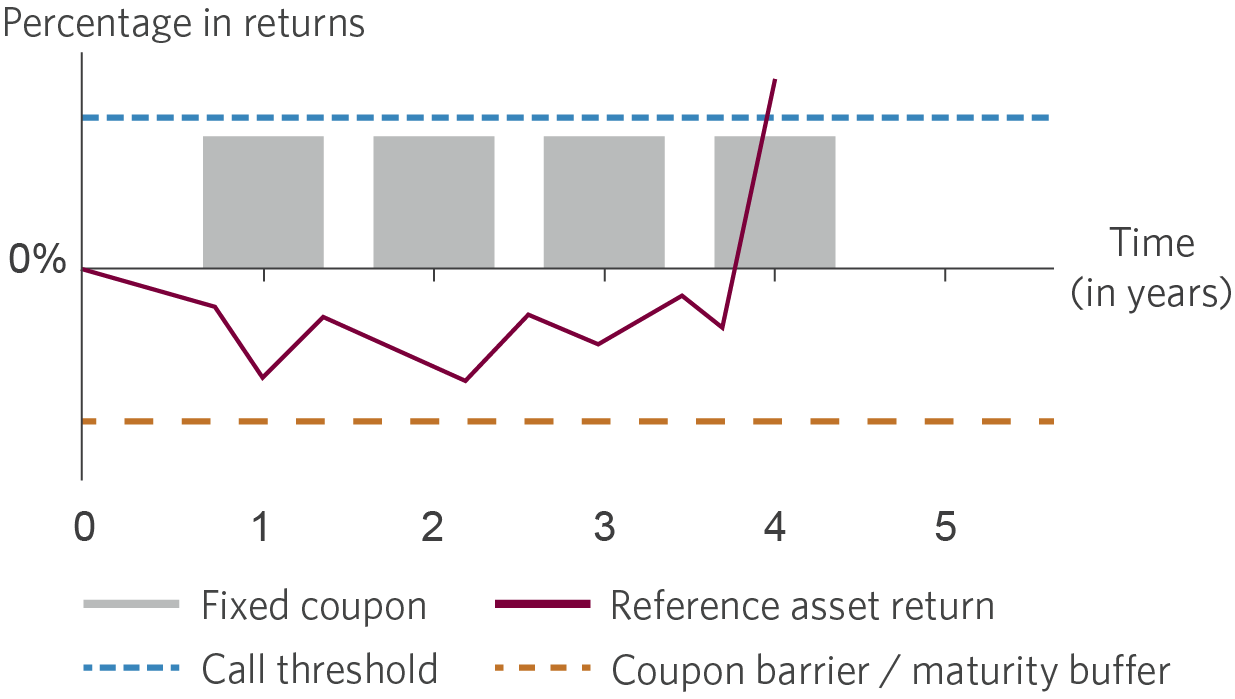

Case 1: Reference asset return is greater than or equal to the coupon barrier and the call threshold on a valuation date prior to maturity.

Note will be called. Investors will receive their initial investment in addition to a predetermined fixed coupon.

The chart illustrates the performance metrics of an autocallable coupon with buffer note over time. The horizontal axis (x-axis) is labeled from 0 to 5, representing years, and the vertical axis (y-axis) starts at 0%, measuring percentages for return. The chart includes the following elements:

a blue horizontal line labeled “Call threshold,” indicating a performance level that may trigger early termination;

an orange horizontal line labeled “Coupon barrier/maturity buffer,” representing a minimum threshold for protection; and

a burgundy jagged line labeled “Reference asset return,” which fluctuates dynamically over time. At time period 4, the white line sharply rises above the call threshold.

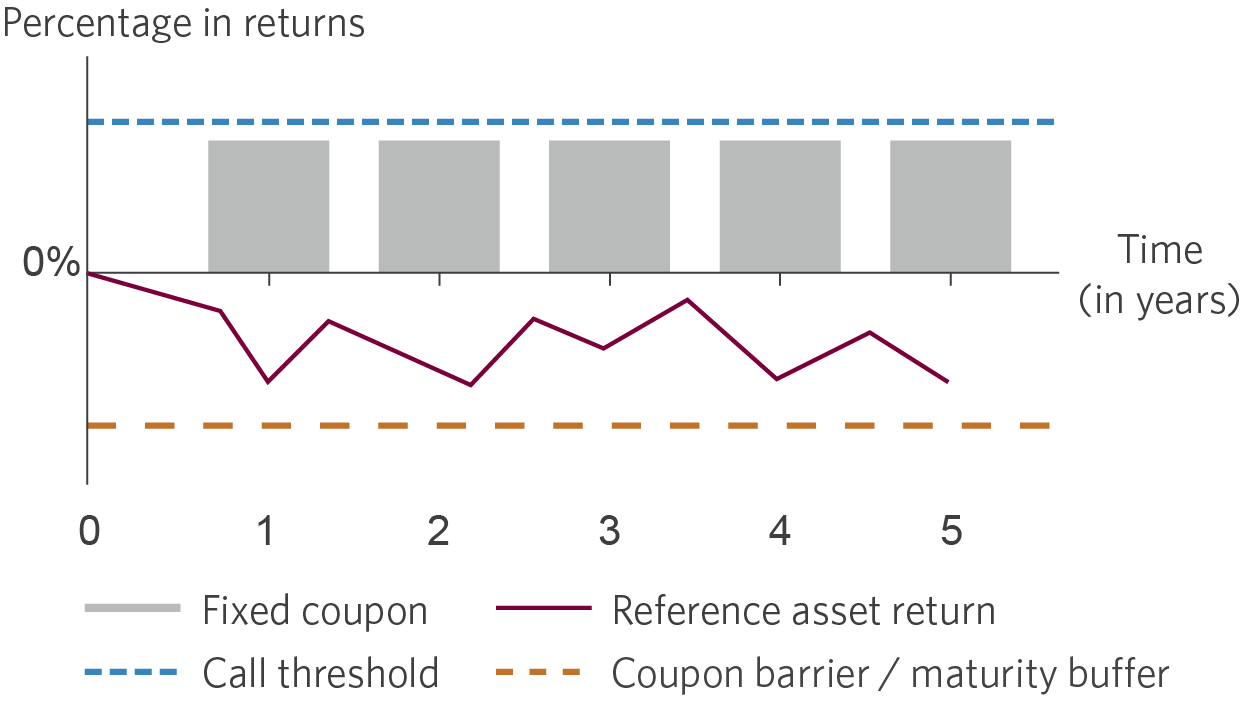

Case 2: Note was not called prior to maturity. Reference asset return is greater than the coupon barrier at maturity and downside buffer is not breached.

Investors will receive their initial investment in addition to a predetermined fixed coupon.

This chart illustrates the performance the autocallable coupon with bufer note over time. The horizontal axis (x-axis) is labeled from 0 to 5, representing the years for the investment, and the vertical axis (y-axis) starts at 0%, measuring percentages for returns. The chart includes the following elements:

grey vertical bars labeled “Fixed Coupon,” representing consistent payouts at each time period;

a blue horizontal line labeled “Call Threshold,” indicating a performance level that may trigger early redemption of the product;

a burgundy fluctuating line labeled “Reference Asset Return,” showing the variable performance of the underlying asset over time; and

an orange horizontal line labeled “Coupon Barrier / Maturity Buffer,” representing a critical threshold below which payouts or protections may be affected.

The chart demonstrates the interaction between fixed payouts, asset performance, and thresholds, highlighting the conditions for early redemption or maturity protection.

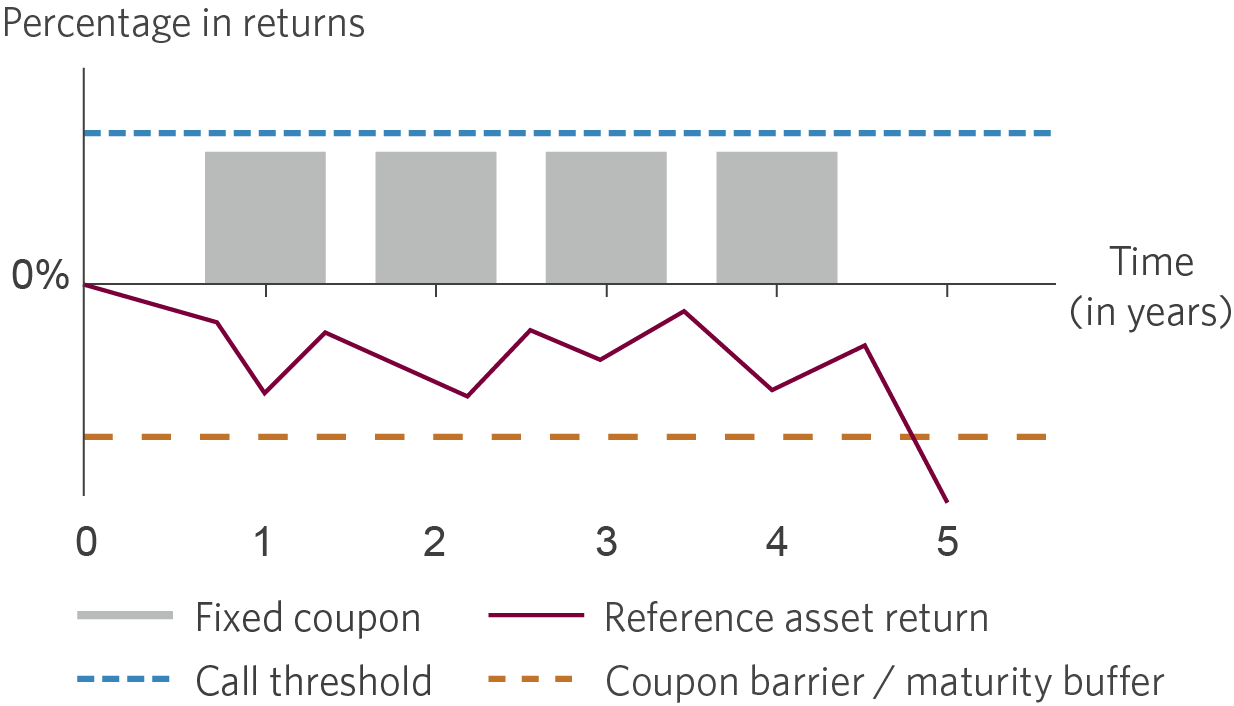

Case 3: Note was not called prior to maturity. Reference asset return is less than coupon barrier at maturity and downside buffer is breached.

Investors will receive initial investment reduced by incremental losses below the buffer and therefore sustain a loss of a portion of their initial investment.

This chart illustrates the performance and structure of an autocallable with coupon buffer note over time. The horizontal axis (x-axis) is labeled with time intervals: 0, 1, 2, 3, 4, and 5, representing the years of the investment, while the vertical axis (y-axis) is centered at 0%, measuring performance or returns in percentages. The chart includes the following elements:

four grey vertical bars labeled “Fixed Coupon,” positioned above the 0% line, representing periodic fixed payments.

a blue horizontal line labeled “Call Threshold,” positioned above the 0% line, indicating a performance level that may trigger early redemption.

A burgundy zigzag line labeled “Reference Asset Return,” fluctuating dynamically across the chart, representing the performance of the underlying asset. The line remains below the blue “Call Threshold” but crosses above and below the orange line.

an orange horizontal line labeled “Coupon Barrier / Maturity Buffer,” positioned below the 0% line, representing a protective threshold or buffer.

The chart visually demonstrates the interaction between fixed coupon payments, asset performance, and the thresholds that determine the product’s return, including elements such as early redemption or maturity protection.

Hypothetical maturity amount calculations

The hypothetical calculations below are provided for illustration purposes only and assume an initial investment of $100.

The hypothetical term of the notes is 2 years with semi-annual valuation dates. The hypothetical call threshold is 5% of the initial reference asset value, and the hypothetical downside buffer is 60% of the initial reference asset value, with a participation factor of 1.67, and coupon barrier of 60%. The hypothetical contingent semi-annual coupon payment is 2.5% (5.0% annual).

Example #1: Reference asset return is greater than the call threshold on valuation date 3

Reference asset return − valuation date 1: −10.00% (coupon payment of $2.5) Reference asset return − valuation date 2: − 50.00% (no coupon payment) Reference asset return − valuation date 3: 6.00% (coupon payment of $2.5) − note called Reference asset return − valuation data 4 : n/a Total coupon payments = $2.5 + $0 + $2.5= $5.0 Variable amount = $0.00 Maturity amount = initial investment + variable amount = $100 + $0 = $100 Total cumulative return = ($105.0 − $100) / $100 = 5.0% The investor received a coupon payment of $2.5 after the first valuation date, and no coupon payments on the second valuation date. After the third valuation date, the note is called and the investor received a coupon payment of $2.5 in addition to the initial investment of $100.

Example #2: Reference asset return is negative at maturity but downside buffer is not breached

Reference asset return − valuation date 1: − 10.00% (coupon payment of $2.5) Reference asset return − valuation date 2: − 50.00% (no coupon payment) Reference asset return − valuation date 3: − 5.00% (coupon payment of $2.5) Reference asset return − valuation data 4 : − 20.00% (coupon payment of $2.5) Total coupon payments = $2.5 + $0 + $2.5 + $2.5 = $7.5 Variable amount = $0.00 Maturity amount = initial investment + variable amount = $100 + $0 = $100 Total cumulative return = ($107.5 − $100) / $100 = 7.5%

The investor received three of four coupon payments in addition to the initial investment of $100 at maturity.

Example #3: Reference asset return is negative at maturity but downside buffer is breached

The investor will receive a coupon payment of $2.5 after the first and third valuation dates, and no coupon payments thereafter. The note is not called prior to maturity. The investor received $83.30 at maturity, which is equal to the initial investment reduced by the product of (i) the reference asset return plus 40%; and (ii) 167%. Therefore the investor will sustain a loss of a portion of their initial investment.